February 21, 2025

Germany on the eve of elections – part 2

Potential coalitions and post-election scenarios.

Last week, I presented in this column , a study by LBBW Research in which we scrutinized the economic policy proposals in the election manifestos of the parties running in the German federal elections. The conclusion: The conservative Union parties (CSU in Bavaria and CDU in the rest of Germany), the Greens, and the liberal FDP offer above-average promising proposals to stimulate Germany’s sputtering growth engine. However, "above average" means just that: better than the mean of all reviewed manifestos; it does not suggest that any one party has discovered the holy grail to resolve Germany’s deep-seated structural growth issues . None has.

Examining economic policy convergence

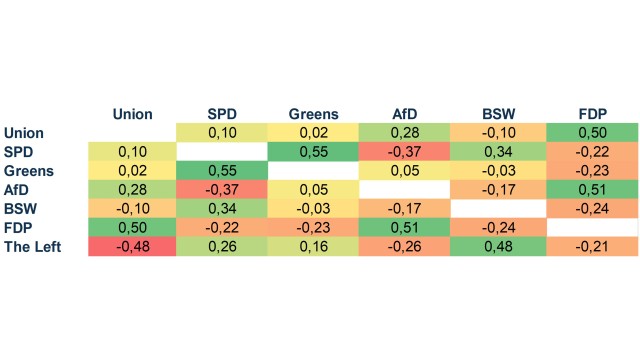

No single party will secure an outright majority. Consequently, a coalition government will need to be formed. It could potentially comprise two or more parties, depending on the number of smaller parties surpassing the crucial five percent threshold needed to gain parliamentary representation. The higher the number of parties in the Bundestag (Germany's lower house), the slimmer the chances for a two-party coalition. Focusing solely on economic policies, the accompanying table illustrates which programs align more closely (high value, green) and which pull into opposite directions (low value, red).

Significant alignment is observed between the Union parties and FDP on one side, and SPD and Greens on the other. So far, so unsurprising. Yet, current polling suggests that none of these combinations will garner a majority. The most plausible scenario points to a coalition led by the CDU with Friedrich Merz as Chancellor, possibly with SPD and/or Greens. Should the FDP manage to cross the electoral threshold, a so-called Germany coalition – comprising CDU (black), SPD (red), and FDP (yellow) – might also be viable. A tripartite coalition would be more complex to navigate, given the moderate programmatic convergence between Union Parties and SPD or Greens, and the particularly stark contradictions between FDP and SPD or Greens. Nevertheless, this could also be turned to an advantage. If, for instance, CDU and the Greens were to form a coalition, each party could contribute its strengths to the coalition agreement: The Union focusing on deregulation and stronger incentives for employment, and the Greens emphasizing investment, education, and integration. The resultant coalition agreement could be better than each party’s manifesto in isolation. Of course, such an outcome would necessitate a spirit of teamwork and humility.

My endorsement for election Sunday

You didn’t seriously expect me to endorse a specific party, did you? Certainly not. However, the Bundestag election is not solely pivotal for the much-needed policy initiatives to give the economy a jolt. Geopolitically, the stakes have rarely been higher. Consequently, the new federal government, irrespective of its composition, needs a robust mandate. A high voter turnout is crucial to achieve this. Hence, my recommendation to the German electorate: cast your vote, even if no party has fully convinced you. Democracy is always about imperfect choices.

A high voter turnout is urgently needed.

Download To the point!

-

287.8 KB | February 21, 2025

This publication is addressed exclusively at recipients in the EU, Switzerland, Liechtenstein and the United Kingdom. This report is not being distributed by LBBW to any person in the United States and LBBW does not intend to solicit any person in the United States. LBBW is under the supervision of the European Central Bank (ECB), Sonnemannstraße 22, 60314 Frankfurt/Main (Ger many) and the German Federal Financial Supervisory Authority (BaFin), Graurheindorfer Str. 108, 53117 Bonn (Ger many) / Marie-Curie-Str. 24-28, 60439 Frankfurt/Main (Germany). This publication is based on generally available sources which we are not able to verify but which we believe to be reliable. Nevertheless, we assume no liability for the accuracy and completeness of this publication. It conveys our non-binding opinion of the market and the products at the time of the editorial deadline, irrespective of any own holdings in these products. This publication does not replace individual advice. It serves only for informational purposes and should not be seen as an offer or request for a purchase or sale. For additional, more timely in-formation on concrete investment options and for individual investment advice, please contact your investment advisor. We retain the right to change the opinions expressed herein at any time and without prior notice. Moreover, we retain the right not to update this information or to stop such updates entirely without prior notice. Past performance, simulations and forecasts shown or described in this publication do not constitute a reliable indicator of future performance. The acceptance of provided research services by a securities services company can qualify as a benefit in supervisory law terms. In these cases LBBW assumes that the benefit is intended to improve the quality of the relevant service for the customer of the benefit recipient. Additional Disclaimer for recipients in the United Kingdom: Authorised and regulated by the European Central Bank (ECB), Sonnemannstraße 22, 60314 Frankfurt/Main (Germany) and the German Federal Financial Supervisory Authority (BaFin), Graurheindorfer Str. 108, 53117 Bonn (Germany) / Marie-Curie-Str. 24-28, 60439 Frankfurt/Main (Germany). Deemed authorised by the Prudential Regulation Authority. Subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority. Details of the Temporary Permissions Regime, which allows EEA-based firms to operate in the UK for a limited period while seeking full authorisation, are available on the Financial Conduct Authority’s website.